1

Cashless society, forced banking, and the War on Cash

33 readers

2 users here now

In many regions people are being forced patronize banks. This community is for that discussion regardless of which side of the war on cash you are on.

The war on cash is war on privacy.

related communities (decentralized only)

closely related:

☠ !cashless_society@nano.garden (ghost node) ← only reachable from instances that federated to that community before nano.garden disappeared

loosely related:

!offgrid@slrpnk.net

!climate_action_individual@slrpnk.net

!fightforprivacy@feddit.ch

!personalfinance@sopuli.xyz

!right_to_unplug@sopuli.xyz

founded 7 months ago

MODERATORS

2

4

1

Russian American ballerina on trial for treason over $50 pro-Ukraine donation faces up to ~~20~~ 15 years incarceration

(www.guardian2zotagl6tmjucg3lrhxdk4dw3lhbqnkvvkywawy3oqfoprid.onion)

5

6

7

8

9

10

11

12

14

15

16

17

cross-posted from: https://slrpnk.net/post/7614616

- The right to be unplugged includes the right to be free from banks as banks increasingly force customers online. There is also a #WarOnCash underway. So even if you make the ethically absent minded decision to pay for your food electronically, the least you can do is pay the tip in cash. (the war on cash is war on privacy)

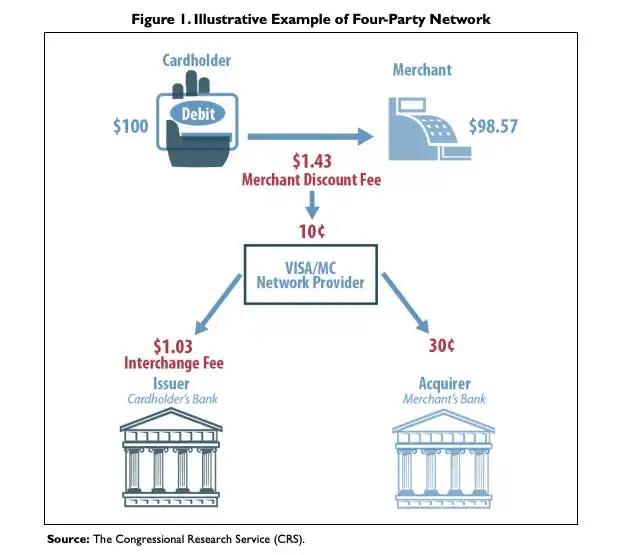

- Electronic tips are also subject to siphoning off by banks. When you tip by card, you also tip Visa, Mastercard, or whatever scumbag credit network is in play because their fee is a percentage of the whole transaction. The electronic transaction may be free to you but it’s not free to the business. I don’t know if the restaurant pays the whole fee and transfers 100% of the tip to the server, or if the server shares the hit. But if this is not McDonalds but some small local business, it’s better to give the full amount to the business anyway.

- Data protection: when you tip electronically, that creates a record not just attached to you but to the server. If you respect /their/ privacy by way of data minimization, you tip in cash.

- Environmental protection: banks are lousy for the environment. (ref: Banking on Climate Chaos, bank blacklist and Wired article)

- Terminal tipping is a swindle (esp. in Europe). Tipping is not only optional in the most pure meaning of the word (not expected), but tipping amounts are lower in Europe meant purely to indicate service quality. Even a tip of €1 is a complement. But terminals suggest American proportions (e.g. 20%). It’s a scam. I think I’ve only seen this in tourist traps. The ownership is happy to make their staff happy by pushing a tip request in a way that deceives the public into thinking it’s out of their hands.. that the technology is asking for the tip. This fucked up scam is training restaurant patrons to overtip w.r.t. the culture (a culture that the locals don’t want to drift into Americanism). In the US it’s not exactly a swindle, but you have less control over the amount nonetheless. Sure most people like the math-free convenience but IMO that does not justify it. And certainly the ~15—25% amounts are excessive when there was no table service.

- Sometimes servers pool their tips to then tip a portion to the kitchen staff who did well enough to make the servers look good. Cash tips make that go smoothly. I was once in a rare situation where I needed to pay by card and I also wanted cash back. The server explained to me they do not give cash back because of that tip pooling that they do, saying that sometimes they do not get enough cash tips to properly treat the kitchen staff.